Below are some of the key comments by individual carriers on their Q3 earnings calls and releases. The breadth and depth of these comments vary considerably by company.

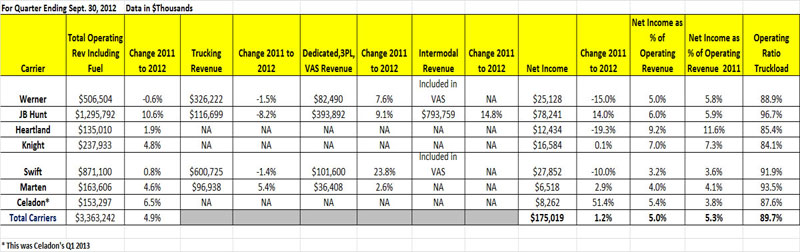

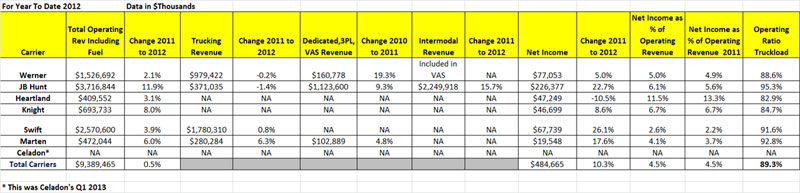

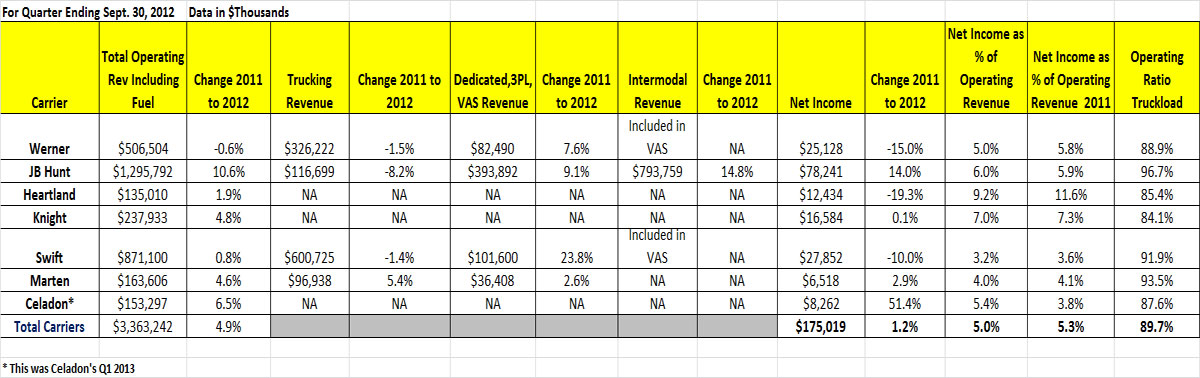

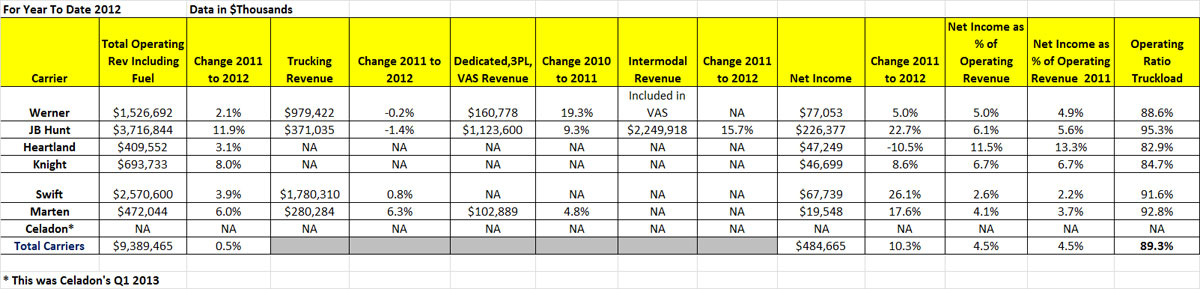

JB Hunt

In its intermodal segment, Hunt saw Eastern network load growth and transcontinental load growth of 22% and 11%, respectively, "primarily from the continued customer conversion of highway traffic to intermodal."

Revenue declined in the truck segment largely because the number of truck in the fleet dropped 9%. The company said that "Rates from consistent shippers increased 2.6% compared to same quarter a year ago."

All told, earnings for Q3 were $78.2 million, up from $68.7 million in Q3 2011. Operating income in the intermodal group was up 25%, providing most of the juice to the bottom line.

Werner

Company said "spot pricing rates trended lower, and the number of special freight projects with customers declined for both our truck fleets and VAS Brokerage unit in third quarter 2012 compared to third quarter 2011."

Its fleet size was down 215 from Q2, to 7110. Werner said this was due "primarily from our

decision to exit certain less profitable customer business during third

quarter 2012."

At 3225, the number of trucks in Werner's dedicated unit now represents 46% of its total.

The company said that "we believe truckload

capacity constraints will continue due to an older industry truck fleet,

the higher cost of new trucks and trailers, significant safety

regulatory changes and a challenging driver market," adding that "Orders for new class 8 trucks have been slowing during

2012. We believe these orders slowed as current freight rate relief is

not keeping pace with the increased costs and capital requirements for

new and much more expensive

EPA

-compliant trucks. The significantly

higher costs of new equipment and related diesel exhaust fluid will not

be recovered through a single year rate review cycle."

It also said that the driver recruiting and retention market became more challenging in

third quarter 2012 compared to second quarter 2012, and that it has been increasing pay for drivers as a result that will result in about a 1.4 cent cost per mile increase in its cost basis - not trivial.

Swift Transportation

Revenue per truck per week increased 3.6% over the third quarter 2011 driven by continued

improvement in asset utilization and revenue per loaded mile.

Swift continues like most to focus on reducing empty miles. Deadhead miles were 11.4% of the total in Q3, which represents the lowest level since 2006.

Swift's intermodal business "continues to grow significantly, increasing 41.5% in the third quarter on a

year over year basis."

The company implemented

a driver incentive program and an owner-operator banded-pay program at the beginning of the third

quarter. "These programs reward our drivers and owner-operators for behaviors that should help Swift

become more efficient as well as enable our driving partners to take home more money," Swift said, in part "leading to improved retention and recruitment levels."

Fleet was down by 738 trucks versus 2011, now to a level of 14,442. That's down 185 from Q2, as the company decided to

"slightly reduce our truck count in order

to better align our capacity with market

freight volumes, enabling us to generate

higher returns on our assets."

As mentioned above about dynamic adjustment, Swift says it "expects to adjust our truck count to match market."

Intermodal, dedicated, etc. saw revenue gains of 23.8% in Q3.

Marten

Marten continues to move to a more regional model, which now represents 72.2% of its truckload fleet compared with 64.8% as of a year earlier.

Truckload revenue was up a strong 5.4%, versus 11.2% for intermodal and 7.9% for brokerage.

Heartland Express

Operating income for the three and nine month periods of 2012 were negatively

impacted by a $5.1 million and $12.9 million decrease in gains on disposal of property and

equipment.

Heartland says that "The industry continues to be challenged by the shortage of qualified drivers and erratic fuel prices."

Company said that it "will continue to take

advantage of the favorable used trailer market throughout the 4th quarter to upgrade our trailer

fleet. As of September 30, 2012 we had taken delivery of 974 new Wabash trailers during 2012

including delivery of 496 during the 3rd quarter."

Knight Transportation

Company noted that "The third quarter of 2012 proved to be more challenging than expected due primarily to eleven consecutive weeks of escalating fuel prices and a slowing economy that yielded seasonally weak freight demand."

Knight's operating ratio of 82.7% for its dry van business was almost 6 percentage points beter than the 88.6 for its refrigerator unit.

Its intermodeal business was up more than 46%, while operating income in its brokerage business increased by 29.7%

''The driver market remains tight and attracting and retaining a sufficient number of qualified driving associates continues to be a concern for the industry, Knight said. "In such an environment we continue to benefit by leveraging our decentralized model and the advantages it provides us with driving associates. As a result, our driver turnover has been trending favorably and is well below what we understand to be the industry average."

Celadon

Company had a strong quarter, with freight revenue increasing 6.4% to $122.1 million in the quarter (its Q1 of fiscal 2013). This was in large part due to some acquisitions over the past year, which increased the size of its fleet by 8%.

Again, Celadon bucked the overall trend, dropping its operating ratio in Q3 to 87.6% from 90.9% yea-over-year.

Profitability was enhanced in part by an on-going program to replace its existing fleet with more fuel-efficient tractors.

Miles per seated truck though were down about 5% from the prior year, "which was a result of the weak freight environment."

Any comments on our Q3 2012 TL Review? Let us know your thoughts at the Feedback button below.

|

{kind=link}

{kind=link}