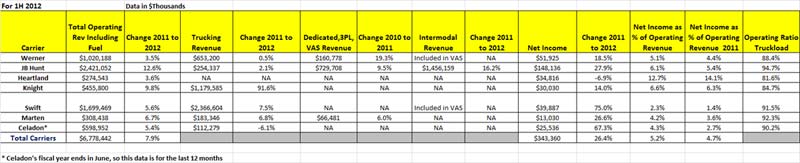

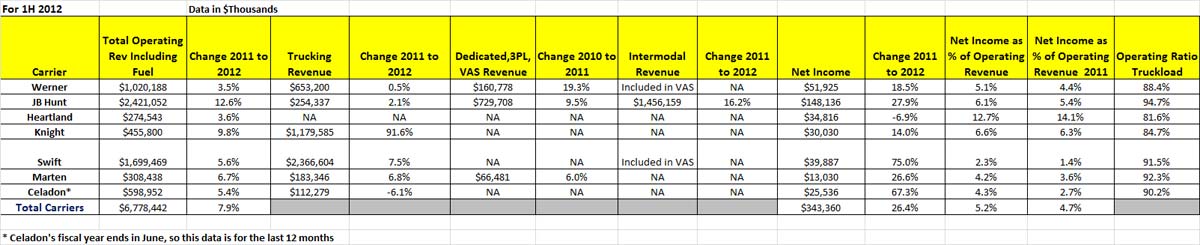

Trucking revenues at Werner were basically flat, whereas its intermodal and other value-added services saw revenue gains of 18%.

So there is a lot of change happening in the truckload sector, not only in terms of what segments are being focused on, but also in terms of service strategy, with several carriers moving to more "regional" orientations.

Below you will find some highlights from earnings calls or press releases.

JB Hunt

Rates per mile, excluding fuel surcharge, increased 3.2% during Q2 for all shippers. Rates from consistent shippers improved 2.5% compared to the same quarter a year ago

At the end of the quarter, Hunt operated 2,396 tractors compared to 2,508 a year ago.

Operating income increased 27% compared to 2011. Favorable changes in freight mix, strong seasonal spot pricing, steadily declining fuel costs and improvements in fuel efficiency were partially offset by increases in driver wages, independent contractor costs, lower utilization and higher empty miles compared to second quarter 2011.

Werner

Said freight demand trends are somewhat favorable to carriers due to supply side constraints limiting truckload capacity and demand generated by economic activity from our customers.

Average revenues per total mile, net of fuel surcharge, rose 2.6% in the second quarter compared to second quarter 2011. It sees a balanced market with respect to freight and trucks during Q2.

Werner says it continues "to be successful in this tightening capacity environment by working jointly with our customers to secure sustainable transportation solutions across all modes and to offset increased rates through enhanced optimization and transportation solutions whenever possible."

Werner was a hundred trucks short of its goal of 7300 due to the challenging driver market intends to maintain its fleet size at approximately this level

It said the driver recruiting and retention market continues to be challenging. Driver pay increased 1.5 cents per mile year-over-year, with Werner saying "an improved freight market, extended government unemployment benefit programs, a reduction in available truck driving school graduates and changing industry safety regulations [CSA 2010] tightened driver supply."

Swift Transportation

Swift saw its operating ratio (operating expenses divided by operaring revenues, one measure of profitability] improve for the 10th time in 11 quarters. Year to date, its OR has dropped 1.4%.

Though it did not break out the numbers separately,Swift said it saw intermodal revenue growth of 50.7% in the quarter versus 2011.

Swift said it continues to shift its business mix from over-the-road linehaul service to dedicated regional service - a major strategy shift.

Freight volumes were "good, not great" throughout the second quarter.

Pay for company drivers is going up about one cent per mile and 1-2 cents for independents.

It is implementing a program that will enable the company will be able to better manage its network and reduce company deadhead by incenting the closest truck, whether company or owner-operator, to haul the nearest available freight, regardless of the length of haul.

Marten

As with Swift, Marten is aggressively moving to a more regional truckload carriage model, saying "We have increased our regional operations to 69.0% of our truckload fleet as of June 30, 2012, from 60.7% as of a year earlier"

It added that "These strategies helped us to achieve our ninth consecutive year-over-year increase in quarterly profitability, as well as our best operating ratio net of fuel surcharge revenue since the second quarter of 2006"

Heartland Express

The company has now achieved ten consecutive quarters of year-over-year growth in operating revenues.

Heartland by far leads the sector in operating ratio, coming in at a very strong 80.9% for the quarter.

Like most others, fuel usage is a big isue at Heartland, with the company saying "We continue to focus on fuel economy and efficiency through the management of idle hours, investment in fuel efficient new tractors, trailer skirts, fuel surcharge billings, and strategic fuel purchasing decisions. These proactive efforts are top priorities in our daily routines."

Driver issues are again the biggest worry.

"Hiring and retaining safe and experienced drivers continues to be the biggest challenge facing our industry," the company said, adding that "We have branded ourselves over the years with our reputation for operating a new fleet of well-maintained equipment, our industry leading driver pay," and more

Knight Transportation

Knight continues to focus on reducing empty deadhead miles, dropping those miles by 3.8% in the quarter to 10.1% of the total.

It is also one of the few carriers to be even modestly aggressive about adding capacity, growing its tractor fleet to 4,070 in Q2 from 3,871 the year before.

''Having a sufficient number of qualified driving associates continues to be a major concern as the driver market continues to tighten," Knight also said

Celadon

Company saw rates increase 4.1% in Q2.

It has also lowered its average tractor age to just 1.5 years, with no truck older than a 2010 model.

It is also working to "streamline our operations to reduce the number of tractors to trailers being operated to support our existing business levels."

Any comments on our Q2 2012 TL Review? Let us know your thoughts at the Feedback button below.

|

{kind=link}

{kind=link}