From SCDigest's On-Target e-Magazine

SCDigest Editorial Staff

Jan.12, 2011

Supply Chain News: Can Procurement and Finance get on the Same Page in Measuring Savings from Supply Management Improvements?

Partial Disconnect between Cash Savings and P&L is Part of the Problem; A Calculation Framework

Calculating the hard value from supply management and procurement efforts is never easy, given the common difficulty in establishing a baseline measure and the numerous external factors that can impact the cost up or down regardless of procurement's efforts.

Still, it is important to make an effort to calculate that value for both the procurement organization as a whole within a company and for individual procurement managers.

One challenge to this effort is that fact that procurement and financial managers are often talking a somewhat different scorebook. While procurement managers tend naturally to think of savings as simple cash improvements, financial managers are often more concerned with the profit and loss statement, using accrual accounting methods.

SCDigest Says: |

|

| It is essential to build a value calculation framework that can work for both procurement and finance, one that includes both cash and P&L dimensions. |

|

What Do You Say?

|

|

|

|

But differences between the two perspectives do not have to be fully reconciled to establish a functional relationship and an commonly accepted measuring systems, say Eric Walsworth and David Yungbluth, procurement analysts at Reed Elsevier in London, writing in the CPO Agenda, a publication of the UK’s Chartered Institute of Purchasing & Supply.

"Procurement can gain endorsement of cost and risk reduction activities, and finance can get useful information to deliver profit improvement," as a result of finding this common ground, Walsworth and Yungbluth write.

Establish a Savings Framework and Definitions

It is essential to build a value calculation framework that can work for both procurement and finance, Walsworth and Yungbluth say, one that includes both cash and P&L dimensions.

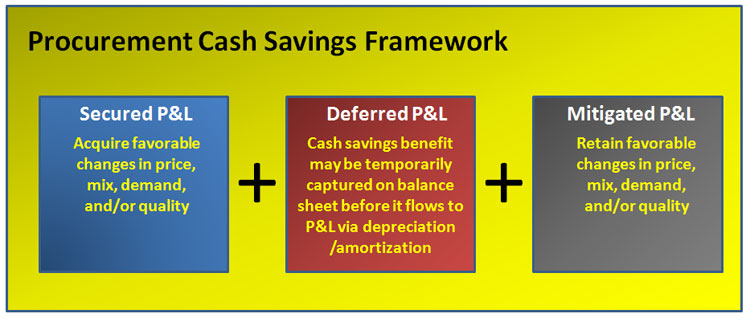

In their model, savings are effectively captured and reported as the first 12 months of estimated financial statement impacts. The relationships between the types of benefits are summarized by the following equation: Cash = Secured P&L + Deferred P&L on Balance Sheet + Mitigated P&L, as shown in the graphic below.

What goes into each savings bucket? According to Walsworth and Yungbluth, each category of savings in the above formula is defined as follows:

Secured P&L Savings: These represent any instances in which favorable terms of purchase are acquired through changes secured in pricing, mix, demand or quality from the vendor. This bucket is a measure of historical or genmeral market prices/terms versus prices/ terms secured from suppliers through negotiation and other strategic sourcing practices. Secured P&L savings can be further categorized as on-going spend measuring period-over-period improvement, or as a one-time spend. This distinction will provide further insight to finance in understanding the impact the savings may have on current and future financial reporting periods.

(Sourcing and Procurement Article Continues Below)

|