2009: a year to remember, and to forget.

As we look back on the year in supply chain, 2009 was period in which the SCM narrative was joined at the hip with the economic one like no other since the start of “the supply chain” era in the mid-1980s.

The reality is that the recession had already started in 2008, especially in the housing and transport sectors, and then was sent into overdrive by the Wall Street collapse in September of that year.

But 2009 was when we really felt the business pain. Below, I will review some of the supply chain impacts from the Great Recession of 2009.

It was “cut, cut, cut” at many companies. Obviously, a number of SCM professionals lost their jobs just as in every other area of business. Projects were put on hold. A panelist at a “Wall Street meets Supply Chain” session at CSCMP in October told attendees that one large retailer had the opportunity and the cash to pursue a network redesign effort they knew would save the company tens of millions of dollars annually, but the project was delayed this year because the company didn’t want to send the signal that it was spending money when everyone else was hunkering down.

Gilmore Says:

|

|

"When you look at nearly all of these numbers, you will see June as the low point, and recovery since then."

What do you say? |

|

Send us

your Feedback here |

|

Many companies took the drop in demand to consolidate distribution facilities. We spoke with one publishing company which moved fast when leases were expiring to combine two distribution operations into a third DC – and in the haste, needing to run three totally separate operations and systems in the one building.

Inventories were whacked with ruthless efficiency – and maybe in some case, perhaps some inefficiency as well. From an anecdotal and personal perspective, it was clear there was a big spike in stock outs at the retail shelf. In late Spring, Best Buy said its sales could have been higher in the first quarter, except for the fact that many vendors had simply not supplied expected merchandise. A Wall Street Journal article around the same time described how the entire electronics supply chain had frozen up for a bit, as a lack of visibility and strong level of fear (and lack of collaboration) resulted in high levels of confusion.

Retailer after retailer, especially in the second half of the year, announced they had pared inventories well beyond the drop in sales. A couple of weeks ago, athletic gear maker Nike said the same thing, saying inventories were down 19%, versus just a 4% drop in sales.

Leading retailers, as well as some manufacturers in consumer goods and industrial sectors, finally started to get serious about reducing SKU counts. Target, for example, discovered it really didn’t need 89 (literally) versions of Pantene shampoo. Some predict total SKU counts at major retailers will drop – perhaps permanently – by 15-20%.

All that said, it might have been a good year for you – if you were in the private label business. Private label manufacturers in general enjoyed a banner year, as consumer and businesses flocked to lower priced goods. This promises to be an even more interesting dynamic going forward.

Relatedly, Procter & Gamble’s generally more “premium” brands caused it to lose some sales, and it released a lower priced (and featured) version of Tide in some areas of the country in response (among other moves). Several luxury retailers also brought more “value” brands to their shelves. The big question is whether this “new normal” in terms of consumer behavior is here for the long term – our bet is yes.

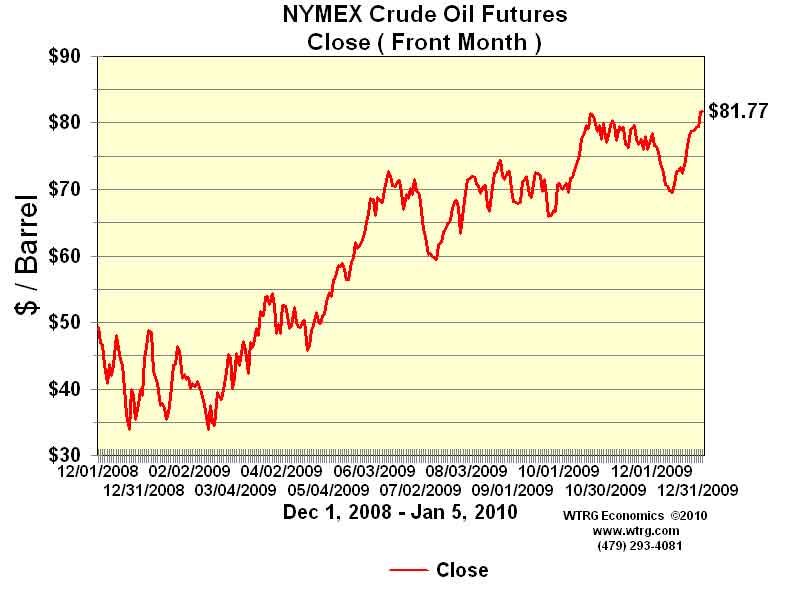

In what may go down as simply one of the weirdest things in history, oil prices collapsed from their highs of $147.00 or so per barrel in July, 2008, to just under $35.00 per barrel in February, 2009. From that point on, however, as can be seen from this chart, oil prices have marched almost in a continuous line back up, now this week inching up over $80 per barrel – in a still weak economy.

The transportation sector took a tremendous hit – and global trade and transportation worst of all. If year over year container volumes are down again in January, as expected, it will be the amazing 31st consecutive month that has been the case. Global Insights is now predicting there will be a year over year gain in February – the first in nearly three years. Incredible.

Truck freight movement also plummeted, as well as rates. The ATA Freight Tonnage Index, which sets year 2000 volumes as the base or 100 level, perhaps surprisingly actually reached its high in June, 2005 at a level of about 122, and has been trending down ever since. In June, 2009 it dipped below 100, meaning we were moving less freight than nine years ago. In November, the mere 3.5% drop in year over year freight movements was “the best showing in 12 months.”

Truckload carriers were said to be moving freight at variable cost or even below. I heard one Werner executive say “the current pricing environment is unsustainable” – but that was in late Spring, and not sure much has changed since then. While a lot of capacity left the trucking market (15-20%), volumes dropped even more. One factor was that because the market for carrier assets (used trucks and terminals) was totally in the toilet, banks were reluctant to pull the plug on carriers to which they had lent money. Thus, many technically insolvent carriers continued to haul, delaying a “market clearing” that might bring supply and demand more in balance.

Ocean carriers were also toiling at rates said to be no more than variable cost, and in an interesting dynamic most were still receiving a series of new “mega-ships” ordered years before when times were good. Hundreds of older ships were parked, some 20% of capacity; apparently, the ocean outside the Port of Singapore looks like a Christmas season mall parking lot in the US, as carriers madly tried to reduce capacity. Most tried to push through rate increases in the second half of the year, with modest success, from what I have heard.

Rail carriers saw volumes plummet too, but largely were able to hold and in some cases even increase rates, as they proudly noted in quarterly earnings calls.

Factory utilization in the US reached a low of just 65%, versus an average over the last two decade of 79.6%, to a level not seen since the Great Depression.

But, like most of the other indicators, that rate bottomed in June, and has risen slowly since. If fact, when you look at nearly all of these numbers, you will see June as the low point, and recovery since then – that is the good news.

On the supply side, companies spent much of the year trying to assess “supplier risk,” and in some cases provided financial assistance of various kinds to keep key suppliers afloat.

In the materials handling industry, the first half of the year was "dismal," as one large vendor told us, and industry group MHIA estimates sales were down 35% in 2009. It is actually surprising more vendors and systems integrators did not go out of business. The second half was better, and most report growing deal pipelines entering 2010.

Other news of note in 2009: the card check union legislation didn’t happen and now may not; cap and trade passed the House but no action yet in Senate; YRC Worldwide, which controls 25% of the US LTL market, continued to teeter on bankruptcy but so far has threaded the needle; JDA Software again is acquiring i2 and this time it should close; Gartner announced it is acquiring AMR Research; DHL left the domestic parcel market at the end of January; China and the US engaged in some saber rattling in terms of trade policy, but so far more posturing than real action; Michael Campion shown the door as head of Dell’s supply chain after a short tenure and major changes; ditto Bo Andersson after a longer run at GM; RFID at Wal-Mart and Sam’s Club ground to a halt.

That’s our 2009 review, and what a year it was. There will be a new business and supply chain "norma"l – looking forward to 2010 and beyond.

Anything to add to our top trends and stories in supply chain for 2009? How do you think this year will impact supply chain going forward? And will 2010 be a better year? Let us know your thoughts at the Feedback button below.

Let us know your thoughts.

Web Page/Printable Version of Column

|

Wright State Univer-sity's Master of Science in Logistics and Supply Chain Management Delivers Direct and Relevant Business Value

Wright State Univer-sity's Master of Science in Logistics and Supply Chain Management Delivers Direct and Relevant Business Value

{kind=link}