From SCDigest's On-Target E-Magazine

Sept. 12, 2012

Supply Chain News: US Manufacturing May be Coming Back - but not Because of Rising Chinese Labor Costs

PWC Research Finds Other Factors Making US Increasingly Advantaged Place to Produce - in Some Industries

SCDigest Editorial Staff

In the latest in a series of studies and reports that have predicted a likely resurgence in US manufacturing, a new report from PWC says there is a good chance the US will see a growth in manufacturing and reshoring - but unlike most others analyses, it doesn't see rising wages in China as a key factor.

Manufacturing has generally been viewed as a bright spot in the overall recovery, growing faster than GDP as a whole and enjoying 34 straight months of expansion since 2009, according to the Purchasing Managers Index from ISM. However, the PMI has shown the manufacturing sector has been contracting, albeit slightly, for the past three months, as the US economy slows in reaction to economic challenges worldwide.

SCDigest Says: |

|

In general, "heavy manufacturers" (chemicals, machinery, paper) will see more advantages for producing domestically, versus "light" manufacturers and those that are very labor-intensive in terms of the percentage of total production costs. |

|

What Do You Say?

|

|

|

|

However, PWC notes that despite the gradual climb back, US manufacturing output is still below peak pre-recession levels, and manufacturing jobs have grown even more slowly than production levels. This, of course, should not be surprising, as factories still well underutilized didn't need to hire back many workers even as volumes expanded - and manufacturers continue to invest in automation.

Nevertheless, "structural changes" that include new dynamics in labor skills, transportation, energy, materials costs, demand, talent, availability of capital, and currency are more likely to drive back or keep manufacturing in the US than wage differentials across the globe.

"Even if an increase in the relative competitiveness of United States labor costs were to unfold, that seems unlikely to be sufficient to result, in itself, in a domestic manufacturing resurgence," PWC says. "Instead, a host of other factors - particularly transportation and energy costs, and currency fluctuations - are more likely the most salient reason United States manufacturers will choose to produce closer to their major customer bases," including of course the US domestic market.

One important driver of domestic manufacturing resurgence could be a renewed understanding of the value of co-locating R&D/engineering with actual production. Examples include Otis Elevator, which cited the importance of co-locating manufacturing and knowledge workers when it recently relocated a plant from Mexico to South Carolina, and Chesapeake Bay Candle when it opened a new factory in Maryland, saying that by embedding R&D into its factory it could achieve market response to changing consumer demand.

The Cost Dynamics in the Steel Products Industry

The report nicely goes into quite a bit of detail in examining total cost dynamics in the steel products industry - companies that fabricate steel into pipes, tubes, etc.

PWC has developed a detailed model that can compare inventory, transportation, and labor costs associated with manufacturing in China versus the United States, when the final goods are sold in the United States.

Inventory cost variables considered in the model for steel products manufacturing included: the level of raw material and final goods inventory based upon estimates of time in transit and safety stock; and the cost of financing these inventories. Transportation cost variables included ocean shipping costs associated with raw materials and final goods, while labor cost variables focused on manufacturing wages in the two countries.

As shown in the graphic below, the US has moved from a 3.57% disadvantage to China across these costs factors in 2006 to a plus 2.06% cost advantage by 2012. The side note says that advantage has likely risen since then, due to a reduction in US energy costs in the past two years, as natural gas prices have collapsed in the US while remaining higher globally.

Source: PWC

In this sector at least, the US is "advantaged" in terms of profitability versus China sourcing.

China Labor Costs aren't the Key

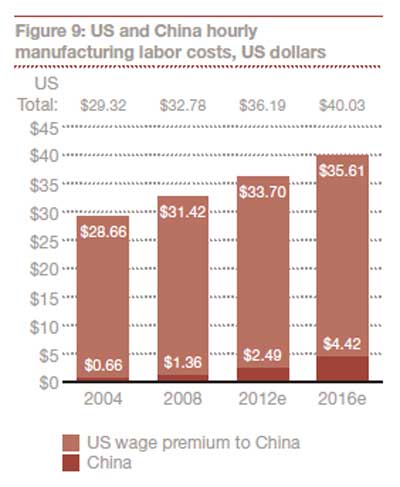

Unlike most other recent studies on this topic, PWC really doesn't believe rising Chinese labor costs are really an important factor in moving manufacturing back to the US, even though research from Boston Consulting Group, for example, recently said that total unit labor costs (wages times productivity) would be roughly equal in between Eastern China and the most competitive areas of the US (mostly in the South) by 2015.

(Manufacturing article continued below)

|