|

January 12, 2017 - Supply Chain Flagship Newsletter |

|

| FEATURED SPONSOR: PROMAT |

||

Register Now for the 2017 Promat Conference |

||

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

From yet another view, US manufacturing was weak/flat for almost all of 2016, based on the monthly output numbers from the Federal Reserve. They were basically flat all year - no expansion, as seen in the chart below. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

More consequentially, as reported just about exclusively by SCDigest, the Federal Reserve in April made a major revision to its US manufacturing data. Among the changes, growth in US manufacturing output since 2013 is now estimated at only about 3%, half the 6% reported previously. That means, as can be seen in the chart above, US manufacturing output is still several percentage points below peak 2007 levels, now 10 years later. This is an under-reported fact. Oil prices had an interesting ride. As can seen in the chart below, WTI prices started the year about $44 per barrel, soon fell to 13-year-lows in February at about $36, rose until June, then stayed in a band of roughly $45-$55 for the rest of the year. Prices jumped to full year highs in late December after OPEC announced planned production cuts. The full year rise was about 21%, with some saying we will see $70 oil in 2016.

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Naturally, US diesel costs roughly followed suit, starting the year at $2.21, falling to $1.98 in mid-February, then ending the year at a high for 2016 of $2.54, meaning the full year increase was about 15%. All told, it was a good year for commodities, which as a group posted their first gain since prices started collapsing in 2011 after a multi-year run, as shown below (the index represents a basket of different commodity types).

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The Scotiabank commodity price index had metals/minerals up about 22% on the year, forest products up 9%, and oil/gas up 15%, though agricultural commodities were down 3.4%, causing reported grief for grocery chains and food manufacturers. The currently strong US dollar keeps a lid on commodity prices here, sends them higher in other countries. There were mixed reports on freight volumes. In their quarterly earnings calls, rail, truckload and LTL carriers almost all characterized freight volumes as weak in each quarter in 2016. The Cass freight shipments index was down year over year every month in 2016 through November, with the exception of October. What's more, in almost every month in 2016 the index was below the levels in each of the years 2013, 2014 and 2015.

For example, the Cass Linehaul Index, which tracks US per mile truckload rates, was barely higher year over year in January and February, then went negative every month after that through November, down in the 1-3.5% range each month. The average rate change was -1.7% for the first 11 months of the year.

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Rail volumes shrank again, with total units down a significant 8.2% for the year. according to the Association of American Railroads. Even once high flying intermodal car volumes were down 1.6% for the year. More telling, in October the Cass Intermodal price index rose modestly year over year after a surprising 22 months consecutive months of price declines.

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The growth of ecommerce sales in the US also rolled on, up 15.5%, 16.0%, and 15.7% in Q1 through Q3, respectively. Ecommerce represented 8.4% of total retail sales in Q3, by the government's calculation, but the way SCDigest figures it, the share is probably now over 10%. Total retail sales were up just 3% in 2016, so ecommerce is rapidly gaining share. Amazon's is somehow growing even faster, with increases in merchandise sales of almost 30% in the US through Q3, and it will end the year with revenue of well more than $130 billion when it reports at the end of the month. For a change, Amazon actually made some profits in the year, $1.6 billion through Q3, but that was still just 2% of sales. What is your reaction of supply chain 2016 in numbers and charts? What would you add? Let us know your thoughts at the Feedback button below.

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

YOUR FEEDBACK

More the great Feedback we received on from Dan Gilmore's First Thoughts column on The Trump Supply Chain?, with his analysis of what we can likely expect in terms of supply chain impact from the Trumpster. First Feedback below from Jon Kirkegaard of DCRA Inc. is outstanding.

Feedback on The Trump Supply Chain:

![]()

Great job bringing this up. lets help the policy create real value from the talk!

Supply chain design and strategy should be used to enable business and government policy goals. As one who has volunteered significant time to use supply chain and advanced manufacturing to promote US jobs I have witnessed the dysfunction. We believed strongly in the concept of using supply chain to create jobs and donated nearly 3 years of time to Texas Governor's office to develop an Industry Cluster Initiative that justified the Texas Emerging Technology fund. Our efforts were key in raising a half billion dollars to fund Texas businesses that would use supply chain strategy and advanced manufacturing to promote jobs.

I considered it a huge win until I saw how the funds were allocated. They all got used to fund any old initiative. Last I checked they were mostly funding business largely importing goods or some politician's friend's supposed cure for cancer. You can only imagine my reaction . We developed a knowledge base as part of this effort and have kept it running since on own www.Texaslcc.org.

So I am obviously refreshed by Mr. Trump's instincts that something has been horribly wrong with our government policy goals and as it relates to cutting the right global deals that support our treasured manufacturing talent.

However, based on my experience, I am very supportive of what we see evolving but am skeptical that the execution can adroitly align with the goals. As has been said many times, the devil is in the details and to say it politely there are many devils in government.

Here are two concepts we believe hold up in the details and are quite simple to understand vs. global supply chain design is not "easy" to understand for the average business person as not very physical, tangible and to them appears far removed from quarterly profits.

First, Promote Postponed Manufacturing in US:

1. Government policy should support and help US companies create a postponed manufacturing or what we describe as an assembly coordination product supply chain. This means the planning bill of materials (components) could be made and purchased in any part of the world but the final assembly is done in US facilities with US personnel. Bottom line benefits it greatly reduces shipping costs, it protects intellectual capital as we are not shipping full designs off shore, it dramatically lowers working capital as the components can be used to make 1000s of times more product variety then just a single SKU wrapped in Styrofoam, stuffed in a shipping container essentially half full of air.

It also helps on US infrastructure side as logically if you are more efficient in shipping it cuts down on port congestion, transportation cube and even assists in clearance as products are simpler to examine.

Most importantly it creates JOBS and jobs if not into every piece of the engineering design they are at least heavily involved in the planning bill of materials of design. For you supply chain planning experts, you know the difference between a design bill of material and planning bill of material. It is this planning bill of material that essentially needs to become inculcated into government policy thus creating jobs. Once you involve personal at all levels more deeply into the product you create millions of paths for PEOPLE to expand career growth, education, innovation, engineering, and production skills. When you buy finished goods wrapped in Styrofoam and set them on a big warehouse shelf you only create jobs for material handlers of which most are being automated.

I have done this analysis for hundreds of US products and have rarely found that the costs are not less for a finished good when you consider customer choice, total supply chain holding and transport costs and in particular when you consider IP protection and balance sheet losses from IP theft.

We even created two businesses that we own and have operated over the past 10 years that use this postponed US assembly model that does create US jobs in manufacturing.

An example of what government could do to support is create a virtual transportation hub to allow the manufacturers to get transport costs down and precisely coordinate arrival based on lead time to their assembly centers. This is the type of 21st century INFRASTRUCTURE we need. A manufacturing nationwide "air traffic control of sorts."

2. Second Key Initiative - Incent Promote Develop Manufacturing in the Inner City

There has been much talk of lack of opportunity in the inner city during this election cycle. Why not use our human resources in the inner city to be involved in the initiative described above (assembly) or in pure manufacturing? Of course this is not without effort - as we can all imagine - but the benefit and rewards could be staggering. If you take a top down initiative such as Mr. Trump has indicated he will do it can happen. Imagine what could happen with the right incentives from government to the private sector to "make things" in the inner city - you could provide the biggest opportunity ladder ever imagined.

Having created two businesses that use this model, I can safely say personnel is a challenge but maybe with the right top down perspective, cheer leading, support it can improve. Lets give fame to value creation in manufacturing vs. pure consumerism.

For those of you who have studied the Chinese model in essence by promoting manufacturing of good for foreign export it is what they have done. They have a coordinated effort including blasting US CFOs with information on cheap labor to the point CFOs don't look at total cost.

Bonus 3rd Initiative - Green “Supply Chain Coordination”:

Lastly, as an overriding theme and as what I personally see as the most GREEN initiative the world could take on is top down support for global supply chain coordination. The amount of resources saved, energy saved, unused product eliminated by even tiny percentage increases in coordination is insanely large then all the "green" initiatives ever proposed. In essence the first initiative above Assembly coordination / postponed manufacturing is just a tiny physical example of a larger scale effort to coordinate global supply chain coordination.

Average business reader is going to get this last topic but readers of your site I think do - and many I think would logically agree that government policy that would support supply chain coordination could really cut out immense pollution, waste and improve lives globally not just in US. It has to start somewhere but the strategy used can and will make a huge difference in realization of benefit.

Jon Kirkegaard

President

DCRA Inc.

![]()

Let's keep this simple.

Unemployment is at 4.9%.

The overall US trade deficit has been largely stable since 2008.

Coal is noncompetitive to gas which currently is plentiful.

For the first time in at least a decade, there is a small decrease in income inequality. (not so meaningful until one considers if tires made in the US that are more expensive, someone will need to be able to buy them.)

Advancement and innovation in supply chain principles made globalization a reality. So why do we want to return to high tariff and protectionism? Those Cuban cars are pretty special, I suppose.

Jerry Saltzman

Director, Global Supply Chain Processes

Pfizer

![]()

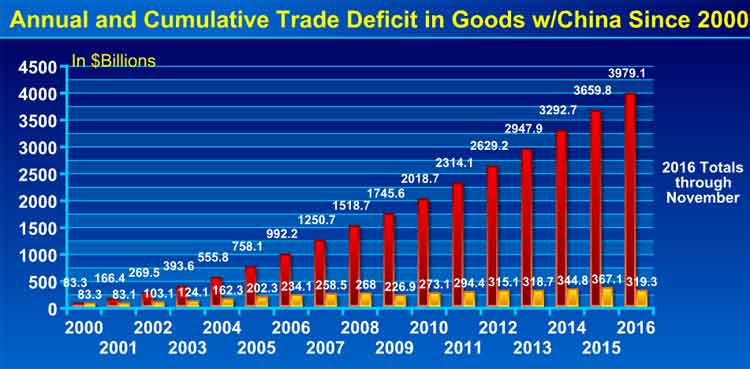

I remember a chart of the U.S. trade deficit with China, where the share of the deficit due to Walmart alone was clearly visible (somewhere in the single digit %). Consumers need to understand that the factories have left the U.S. because consumers want to buy T-shirts for $9 and DVD players for $39.

PATRICK LEMOINE

Vice President, Product Marketing

E2OPEN

SUPPLY CHAIN TRIVIA ANSWER

Q: By how much are US per mile truckload rates up since the start of 2005?

A: About 24%, according to the Cass Linehaul Index, or only about 1.8% per year.

| © SupplyChainDigest™ 2003-2016. All Rights Reserved. SupplyChainDigest PO Box 714 Springboro, Ohio 45066 |

POWERED BY: XDIMENSION

|