|

July 14, 2016 - Supply Chain Flagship Newsletter |

|

| FEATURED SPONSOR: APEX SUPPLY CHAIN TECHNOLOGIES |

|||

|

|||

Making Spaces Smart: Automated Restock Alerts Keep Lines Up and Running |

|||

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

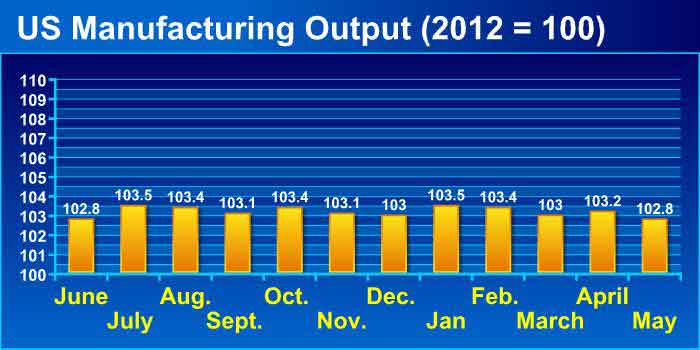

But US manufacturing output numbers have been flat for a year, according to the Federal Reserve estimates, with the index numbers as shown in the chart below relative to the baseline year (index = 100) of 2012. As can be seen, there has been no increase in 2016, and the scores around 103 mean just 3% growth in output since 2012 - less than 1% per year. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Oil started the year continuing a plunge that began in 2015, falling to the low 30-dollar range in January, as gas and diesel prices followed suit. That as OPEC decided to keep pumping despite the low price to drive out US frackers. That strategy partially worked, and oil started to climb again in April, almost hitting $50 mark for a bit, now settled in at about $45 per barrel. Diesel prices fell nationally to just below $2.00 per gallon in late February, increasing to a still modest $2.40 or so recently with the rise in oil. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

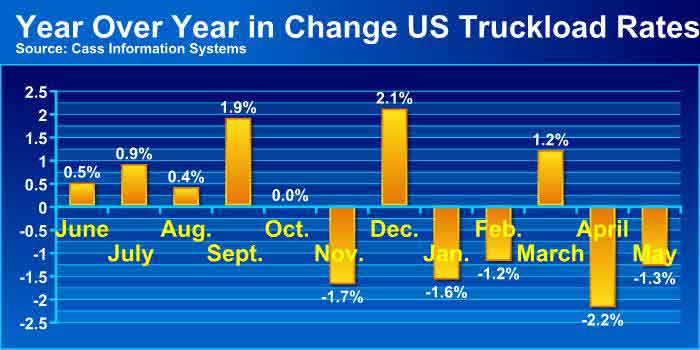

Those lower fuel costs and a generally weak freight environment made it good times for shippers. The Cass Linehaul Index, which measures per mile US truckload rates before accessorials, fuel and other charges, fell four out of the first five month year over year, a big change from 1H 2015 when rates rose rapidly. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Meanwhile, through May the Cass Intermodal pricing Index has fallen an incredible 17 consecutive months. It was great times for global shippers too, with the Chinese Containerized Freight Index continuing to fall, as shown below, down to 650 or so recently from a recent high of 1110 in 2014, as rates are below variable costs for many/all container lines, leading to the recent consolidations. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

I have more but am out of space. Hope you enjoyed this review in numbers and charts.

Anything we missed? What do these trends tell you? Let us know your thoughts at the Feedback button below. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

YOUR FEEDBACK

Catching up on a variety of Feedback this week, starting with an older response from Marc Wulfraat of

MWPVL International on why truck trailers that we hadn't placed here yet that we thought was worth publishing, plus several others on various topics.

Feedback on Why Amazon is Acquiring Truck Trailers

![]()

Our interpretation of Amazon's acquisition of trailers is:

1) The company is seeking to improve how it moves merchandise between its internal network of distribution centers (replenishment center to fulfillment center; fulfillment center to fulfillment center; and fulfillment center to sortation center).

2) The purchase of trailers allows Amazon to stage trailers at these facilities to allow flexibility in terms of timing of loading operations similar to having a drop trailer program with a supplier. It enables Amazon to secure trailer capacity within its own network which implies a greater degree of control as opposed to relying on third party carriers. Bottom line it provides more control over transportation operations.

3) There is likely a modest cost savings associated with this move. Amazon is not buying tractors and therefore does not carry the burden of having the insurance obligations that a trucking company pays for.

4) There is a side benefit in that the trailers serve as giant moving marketing billboards so free advertising doesn't hurt the cause.

5) Perhaps the most important benefit is one that has nothing to do with transportation and everything with Amazon Prime Now. There is a possibility that some of these trailers can be used as “warehouses on wheels”. Companies who sell off the back of a truck understand how this works. The trailer is loaded up with hyper-fast SKUs that are frequently ordered from fulfillment centers. The trailers are loaded in such a way that the driver can access the goods from inside the trailer. Trailer parks in a staging location near an urban center.

Orders are picked off the truck and delivered by localized resources to consumer doorstep in under 60 minutes. Think of this as extending the Amazon Prime Now network without having the Prime Now buildings in every location that needs to be served. This could be a Trojan horse that enables 60 minute service levels to many smaller and midsize cities that make up a substantial portion of the population. Amazon is famous for thinking out of the box so call me crazy but could this be yet another way to move goods to market?

Marc Wulfraat

President

MWPVL International Inc.

![]()

Feedback on Understanding the Gartner Top 25 Supply Chain List

![]()

In regards to the Gartner Top 25, I think it is the gold standard that all companies desire to be aspire to. I have participated in the voting for many years and think the methodology includes many factors, some Supply chain centric, some not.

An enhancement would be to add additional Supply Chain KPIs Key Performance Indicators. There are plenty to choose from, but adding more of these critical measurements would truly indicate the real performance of a company's Supply chain expertise. And that is what the Top 25 is all about.

Tom Dadmun

Supply Chain VP, retired

Adtran

![]()

![]()

The metrics used are inward facing. I suggest that Gartner should also use customer facing metrics like on time shipment or Perfect Order fulfillment (both SCOR metrics)

Blair Williams CFPIM, CSCP

NYU

Editor's Note: The challenge is Gartner gets its performance measures, such as ROA or inventory turns, through public filings. The metrics suggested in these two feedbacks, which would be great if possible, are not available in those filings and would have to be self-reported by companies.

In addition, most companies on the list have multiple divisions/SBUs, etc., so the question would be how to come up with a single number, which usually isn't calculated across these units.

![]()

Feedback on Risk Management

One of my colleagues from Cranfield University used to conclude her half-day session on the management of risk, resilience and vulnerability in the supply chain with the following conclusions:

• No system is invulnerable

• Risk, a problem to resolve, but never solve

• Identify what you can and take a position

• Manage or mitigate as appropriate

• Beware the strategic disconnect

• Forewarned is forearmed

• A case for the rehabilitation of ‘slack'

• Creeping crises were systemic risk in action

• Dialogue between industry & policy makers helps

• Political and commercial aims often diverge

Above all - UNDERSTAND YOUR ASSUMPTIONS.

Bearing in mind the context that the audience was defense and military related and therefore focused on capability rather than availability I found her conclusions both pragmatic and intellectually challenging. In particular the remark concerning "slack" struck home because as a former logistics practitioner and an industrial engineer I had wavered between always having a little spare capacity up my sleeve and an almost genetic disposition to cut out waste.

As an academic she was posing the question: should we not make a case for slack (although recognizing that the term itself was not really sufficient to fully explain the concept)? Events in recent years would support this view. The question is how should one program in slack in such a way that it is not redundant.

What is the mix of physical assets, human resources, systems flexibility, etc., that is required to reduce vulnerability and ensure resilience. How does one convince a line manager, senior VP, CFO, of the merits of such a seeming heresy in these days of austerity and short termism?

I think that this is an issue worth debating and finding solutions - SCDigest would seem a possible forum.

I hope this gives you a little more background without going into it in too much depth. I happy to answer more questions as and when you have them.

David Macleod

Learn Logistics Limited![]()

SUPPLY CHAIN TRIVIA ANSWER

Q: What country has the highest manufacturing robotic density - number of robots per 10,000 manufacturing workers?

A: South Korea, at 347, according to the last estimate from the Int'l Robotics Federation, just ahead of Japan (339). The US is 7th at 135.

| © SupplyChainDigest™ 2003-2016. All Rights Reserved. SupplyChainDigest PO Box 714 Springboro, Ohio 45066 |

POWERED BY: XDIMENSION

|