I am often torn (as I suspect many of our readers are as well) when pondering the state of US logistics infrastructure.

On Monday, president Obama called for investment of an additional $50 billion on top of existing budgets to improve infrastructure in three areas (roads, runways, and rail lines), and creation of a "Infrastructure Bank" that will keep more permanent focus on this issue and in theory a more steady stream of funding for years to come.

So the questions are, it seems to me:

Gilmore Says: |

Being "competitive" as a country, and the role of logistics infrastructure in that equation, is not about being better at getting Chinese made goods to US retail shelves faster. Being "competitive" as a country, and the role of logistics infrastructure in that equation, is not about being better at getting Chinese made goods to US retail shelves faster.

Click Here to See

Reader Feedback

|

- What is the true state of US logistics infrastructure now, really?

- How can you most rationally separate "consumer" versus business issues?

- How big a factor is infrastructure in a country's global competitiveness?

- How should any additional investments dollars best be spent?

I am going to start with question #2 first, actually, because there is no question that from a non-business perspective, congestion and safety are clear and rising issues. Traffic congestion is most major US metropolitan areas is miserable, adding in effect many minutes or even hours to the work day for millions in addition to the aggravation. The aging bridge system - soon forgotten, it seems, after the bridge collapse in St. Paul in 2007 - probably represents real danger to drivers, and that danger increases each year as repairs are bypassed. Lack of investment in airport runways means that the slightest hiccup in the weather brings painful delays throughout the US air systems, as many of us experience regularly.

While there is some overlap with business logistics concerns in these areas, primarily in the congestion in cities that can certainly delay local deliveries but also truck traffic passing through those areas, it still seems to me that we need to sort of compartmentalize potential investments into those that are primarily consumer oriented, primarily business oriented (e.g., ports) or both.

In terms of the state of US infrastructure, I think in reality there are mixed signals.

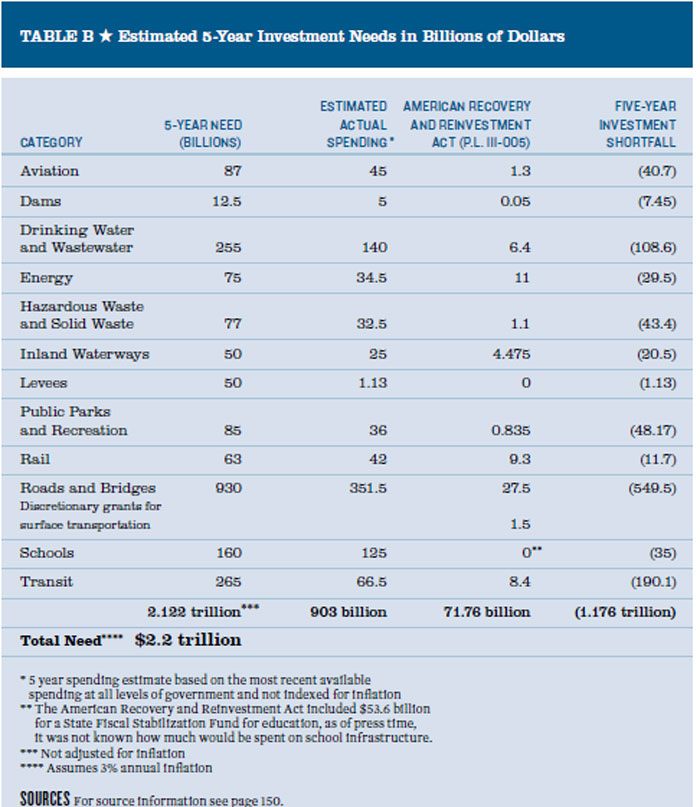

The latest "report card" on US infrastructure from American Society of Civil Engineers in 2009 gave the country a grade of D, and called for investment of some $2.2 trillion over five years to address the issues. With planned spending of roughly $1 trillion in that period, that leaves a shortfall, the ASCE says, of $1.17 trillion (that's with a T). (View ASCE chart - you may have to expand magnification).

A few points: (1) you could say the ASCE has a strong vested interest in greatly increasing infrastructure investment; (2) the numbers include many infrastructure categories, including parks and levees, though it identifies a shortfall of $550 billion in roads and bridges, by far the largest gap; and (3) as per my question #4, since under the best of circumstances nothing like an extra trillion dollars is going to be available, what areas are really most critical (remembering to consider consumer versus business logistics focus)?

I went around on this last year a bit too, and frankly could hardly find anyone who could intelligently comment on that specific question. If you can, I would love to hear from you.

In 2006, then UPS CEO Mike Eskew gave a speech on the US logistics infrastructure deficiencies that drew a lot of attention. Eskew commented that "What's shocking, quite frankly, is the inability of our transportation infrastructure to keep up with the normal day-to-day stresses imposed upon it," said UPS CEO Mike Eskew. "Our highways, waterways, railroads and aviation networks are simply not keeping up with ordinary demands."

In 2009, with Eskew now retired, I inquired into UPS as to what areas, specifically, limited additional investment dollars should go. I ultimately talked to UPS spokesman Malcom Berkley, a good guy and straight shooter, who didn't want to offer much in the way of specifics about how to most effectively allocate scarce dollars, other than to say attention should focus on "bottleneck points."

What he did say , however, was that the silo-oriented approach in Congress needed to change.

"We don't want there to be a highway fund, and a rail fund, and an airport fund," Berkley told me. "We need a single, integrated approach to the infrastructure problems."

Which, one could easily argue, an "Infrastructure Bank" could provide if it was well structured and was run effectively - as always in Washington, large hurdles.

The funny reality though is that in talking to many supply chain executives, I find very few to the point of none really talking about infrastructure as a concern, short term or long term. The one exception - the 2005-06 port delays, especially in Long Beach/LA. But there it was very focused on improving container unloading capacity and speed; Asian ports last I looked were still significantly more productive than the best the US has to offer, as many noted at the time. But a combination of multi-port strategies by many importers, some efficiency gains at US ports and programs like PierPass that better distributed container volumes in LA/Long Beach across the full day, and of course more lately the recession and steep drops in container volumes means - at least for the present - port throughput is at best a modest concern for most shippers.

Despite perceived infrastructure weaknesses, general improvements in transportation effectiveness overall have enabled many companies to build fewer, larger DC further away from customers and still meet delivery requirements. Rail carriers in general continue to make improvements in speed and consistency, largely through software improvements and centralized network control.

In its second global Logistics Performance Index last year, the World Bank rated the US as having the seventh most efficient logistics infrastructure, behind (in order) Germany, Netherlands, Norway, Singapore, Japan and Switzerland (all much smaller land masses than the US). To add more perspective, top-ranked Germany had a score of 4.34 out of 5, versus a 4.15 mark for the US. (See World Bank Releases Latest Ranking of Logistics Performance by Country.)

So who is right? The Society of Civil Engineers, or the World Bank analysts? Is the problem not the present, but the future?

We can all agree a lousy infrastructure or related barriers to logistics efficiency can cost a country dearly in dollars and competitiveness - witness Mexico and India as two big time examples.

Certainly port congestion and uncertainty in the US did and could again impose real costs on companies and force them to bulk up on inventory. And twice over the last few years, we've seen US exports hurt by trouble getting containers or outbound shipment berths - though these were not really "infrastructure" issues.

And it seems to me how much you might be tempted to spend to improve the business logistics infrastructure here is directly related to how manufacturing will ultimately fare in the US. The idea of being "competitive" as a country, and the role of logistics infrastructure in that equation, is not about being better at getting Chinese made goods to US retail shelves faster, but about lower costs for US manufacturers so that they can better compete here and overseas against global competition. Add to that this question: how much would improved infrastructure here change the overall offshoring dynamic?

Unfortunately not much, I think, though nascent signs of some return on production to US territory are encouraging.

Lastly, I will again note as I did last year that it is most likely that rises in diesel taxes will be the key source for any significant increase in business logistics infrastructure spend. At some point, clearly the cost of that increase starts to outweigh the business benefits. Everyone wants improved infrastructure if someone else pays for it, but if shippers must foot the bill, how far would they really go? I also wonder if logistics professionals in major cities wouldn't really opt for less congestion on the way to work than for really improving rail coverage across the US, if they had the choice.

More questions than answers here I realize, but I am just trying to frame the questions and debate logically. Would love your thoughts on this.

What grade would you give the US logistics infrastructure today, and why? Should we be very concerned about the future, given current trends and dynamics? Do you like how we have framed the issues - or is Gilmore all wet? Let us know your thoughts at the Feedback button below.

|

{kind=link}