From SCDigest's On-Target E-Magazine

- May 23, 2013 -

Logistics News: Q1 2013 Rail Carrier Review

Rail Carriers Contine to Growth the Bottom Line Despite Soft Volumes, as Pricing Power Remains

SCDigest Editorial Staff

We're back as usual every quarter with our review of the results and comments from leading public transportation carriers, as the last of them finished up their earnings reports in the last few weeks.

SCDigest Says: |

|

| As shown in the chart below from CSX, on-time originations and destinations have both seen dramatic improvements in recent years.

|

|

What Do You Say?

|

|

|

|

Last week, we took a look truckload sector (see Q1 2013 Truckload Carrier Review.)

This week, we'll review results from the four major public US rail carriers, and then next week we will present similar data and analysis for less-than-truckload carriers.

For three of the four quarters we provide results for both the just closed quarter as well as year-to-date numbers, but as nearly all carriers operate on a calendar year basis, after Q1 the quarter and year-to-date are obviously the same, so the latter is unneeded.

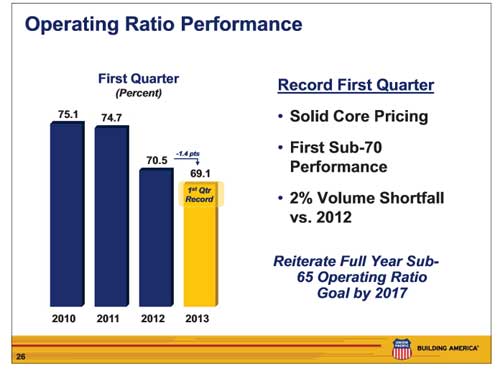

For the rails, the story in Q1 was that despite flat or even slightly declining carload voumes for the quarter, the rail carriers were mostly able to drive up profits and improve their operating ratios (operating expenses divided by operating revenues) nevertheless, driven by continued pricing power and a relentless focus on network efficiencies.

As can be seen in the chart below, operating revenues were up among the four just over 1%, and carload volumes ranges from a +3% gain at Norfolk Southern to negative 2% at both Union Pacific and CSX, as a slow economy, continued steep drops in coal shipments, slow agricultural shipments for most of these carriers resulting from the Midwest drought last summer combined to offset growth in intermodal cars.

Nevertheless, net income from the four in aggregate was up 9.6%, led by Kansas City Southern's 34% gain, while Union Pacific and Norfolk Southern saw net income grow in the 10% range.

That's not surprising given that in general operating ratios continue to fall, down in an unweighted average of 71.2 in Q1 from the average in Q1 2012 of 71.5. The drop would have been still more except for Norfolk Southern's 1.5 percentage point rise in OR. Union Pacific broke below the 70% level in Q1.

Q1 2013 Rail Sector Results

See Larger Image

Carriers that provided pricing numbers all said core price gains were about 4% in Q1, and several said they expect to be in that same range for the rest of the year.

(Transportation Management Article Continued Below)

|

{kind=link}