|

Most of you that have real jobs may have been able to somewhat insulate yourselves from the market and economic turmoil of this week by staying busy at what you do, but not me. At our relatively small business I have the luxury, of a sort, of keeping CNBC on in the background as I do what I do. It was on most of this week - it obviously wasn't pretty, but I couldn't turn it off.

Given all that, I just can't get my head around core supply chain topics this week, and am going to offer some perspective on what is going on in the economy and markets, and try to tie it to the supply chain impact at the end.

Gilmore Says: |

My economic prediction: this current crisis will pass and things will marginally stabilize, and the economy will muddle along, with the idea of higher growth pushed further out. My economic prediction: this current crisis will pass and things will marginally stabilize, and the economy will muddle along, with the idea of higher growth pushed further out.

Click Here to See

Reader Feedback

|

This week and how all the news pulled me towards the overall economy's fortunes and away from supply chain reminded of two similar but very different situations I have been in over the past 12 years or so, First was in 1999, where I was an industry analyst and in Philadelphia along with some 14,000 others for the SAP SAPHIRE conference. On the second main day, a major hurricane (Emily?) had made it that far up the East Coast, and soon was battering Philly with blinding rain and winds. You were sitting there in a presentation trying to pretend even to yourself you were really interest in what was new in the APO module, when all you could really think about was how you could possibly get out of town. Ultimately, I had to drive to Pittsburgh to get a flight home.

More similar to this week, in 2008 the CSCMP conference in Denver was the exact same week that Lehman Brothers failed, and the stock market was declining 500 points a day. I remember interviewing CSCMP CEO Rick Blasgen, and I think he had a pager or something that was updating him on the market, and several times as we were setting up and concluding he would look down and say something like "market's down another 180 points" or whatever it was. It was again a little hard to really pay much attention to say the presentation on keys to network optimization success with all that going on.

So are we back to 2008? I don't think so, but it is going to be tough slogging nevertheless.

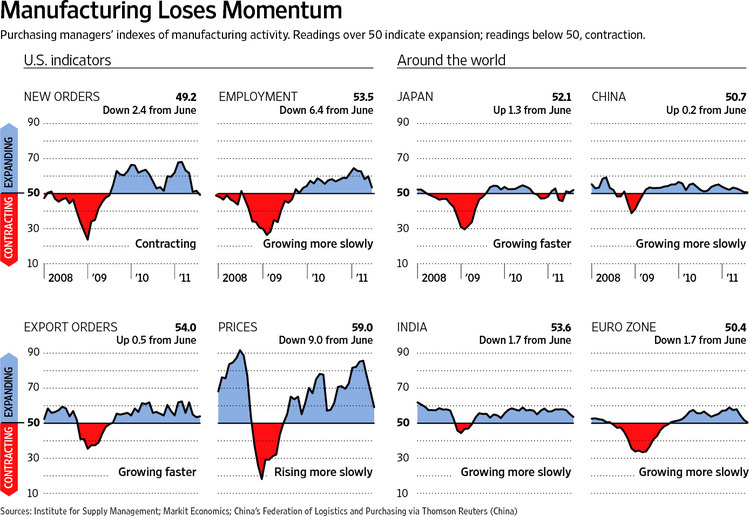

The signs of a weakening economy were already there. Below, you will see the graphic we posted last week, prior to the market debacle that started on Friday, and you can see the weakness showing up in measure after measure in recent months, especially in June. (Remember, with the PMI measures anything over 50 indicates expansion, under 50 contraction, but you also need to look at the direction of either. We are seeing dramatically slowing expansion of late.)

View Full Size Image

On top of that, you have a credit and banking crisis in Europe that may explode at any time. Jim Cramer thinks it can be managed, but with some pain, but really no one knows. I believe there will be some major bad news and a major inflection point somewhere in the next 6 months or so over these issues. The German people will simply say enough of bailing everyone else out. There is much political tension there over the path forward.

China has some major bubbles of its own, with huge government debt at the state/local levels, an economy only moving along nicely until recently due to (1) massive infrastructure spending that is not sustainable and (2) their huge positive trade balances. Inflation is rising there at more than 6%, the debt binge is coming home to roost, and Western governments are tired of footing the bill. Things will change there, maybe for the long term good but not necessarily in the short term.

Riots in the UK and elsewhere, though it appears by hooligans rather than real social unrest. Nevertheless, a well known Democratic pollster said this week Americans are in a "pre-rage" state not seen in decades.

On the good side, oil prices have slid mightily, down to $80 per barrel or so. That will be a sort of natural stimulus for consumers and business that will fight the downward economic pressure.

Many corporations have been highly profitable for 18-24 months, due to cost cutting, and are stuffed with cash. If the law is changed to allow them to bring home cash held offshore at acceptable tax rates (US companies pay taxes in the local countries; the US is one of the few that wants to tax them again for repatriating those profits), that would put even more cash in US business checking accounts. The point just is that many firms will be well funded to ride out a downturn, unlike 2008/09. Credit should not be that hard to get, certainly in comparison to how credit disappeared in 2008.

I just do not see the stock market collapsing to the 6500 type level we saw then. While we are unlikely to fully spring back to where we were soon, the "lost wealth effect" shouldn't be nearly as bad this time. That opinion and $4.00 will get you a small Starbucks.

So, where is the intersection with all this and the supply chain? My thoughts.

- The period of extreme volatility in demand and input commodity prices is going to last well into the future. Companies need to plan networks, response capabilities, hedging strategies, etc. explicitly with the recognition of this volatility, and how it can be best managed. Few companies really do this, actually.

- Relatedly, we are in an era that will likely last in which oil only declines along with slow economic growth or financial panic. Economic good news means higher oil prices, and really good news means prices easily over $100 and higher. The idea of good economic growth and even medium oil prices is largely gone until/unless there is a change in energy technology, policy, etc. In turn though, high oil puts a damper on the global economy. What a scenario.

- We have to expect right now that most decisions in terms of investment, hiring and other supply chain initiatives will be put on hold, awaiting a more definitive view of where we are headed. Vendors close to getting a signature on a contract better move really, really fast.

- I may be wrong, but I think many supply chains have cut staff so far, mostly in 2009, that barring a collapse in volumes (which I do not expect), I am just not sure how many more could be let go and still keep the freight moving.

- Corporate cash positions and much better credit availability should mean the extreme pressure we saw in 2008-09 to slash inventories somewhat indiscriminately will be much lower. That said, with slow top line growth continuing/extending , companies as usual will turn to the supply chain to reduce costs to shore up profit, with increase urgency versus the past year.

- While there are troubles in many emerging economies, including China and Brazil, the belief window of slow growth in Western economies will be extended, leading companies to focus even more fervently on expansion in emerging markets chasing a bull market somewhere.

- I would say there is a 33-50% chance the Euro doesn't make it. That would mean companies would need to recalibrate currency issues country by country there again, and many Euro countries would devalue their currencies to try to rev export business and reduce the impact of their debt levels. But this would take some time to play out. China desperately wants to change away from the dollar as the world's reserve currency, which in the end would result in more loss in the value of the dollar and make imports more expensive, but I don't think given the turmoil this really can happen any time soon.

- There will be a renewed round of tension between retailers and manufacturers in terms of pricing, as CPG companies are pressure by high/rising input costs (driven in large part by weak dollar) and highly competitive cost pressures on the shelf.

My economic prediction: this current crisis will pass and things will marginally stabilize, and the economy will muddle along, with the idea of higher growth pushed further out. If we have a recession, it will be relatively mild, if painful given the already weak condition of the patient (but importantly not many large companies). The global system will be shocked again in the next 6-9 months when the Euro debt mess comes to some sort of head.

What are your predictions into how this will play out in the economy and the supply chain? Agree or disagree with Gilmore's view? What are the other impacts you see on the supply chain? Let us know your thoughts at the Feedback button below.

|