Nonetheless, clearly DSD offers the potential to reduce cycle times and take substantial amounts of total supply chain inventory out of the pipeline in many categories. Nonetheless, clearly DSD offers the potential to reduce cycle times and take substantial amounts of total supply chain inventory out of the pipeline in many categories.

In addition, DSD programs generally result in the manufacturer/distributor getting a better view of “true demand,” through the route agents taking inventory at the shelf and providing near real-time feedback on sales levels and current inventories that traditional systems and processes have just not well managed to achieve yet.

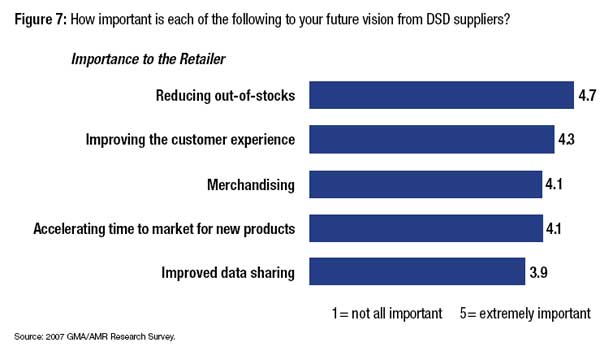

“The time to sense shelf movement and translate this true demand to an order is where DSD processes excel,” according to a GMA report. “With changing demographics and localized assortments, for the retailer, this capability grows in importance as they execute programs to customize the shopper experience—new store banners, localized assortments, and specialized display programs—to shape demand with minimal out-of-stocks at the shelf.”

Store Practices – and the Green Supply Chain – Can be Barriers

Sometimes, traditional store practices and constrains can get in the way of maximizing the results from DSD, however. For example, many retailers still limit receiving hours to Monday to Friday in many stores, even as the percent of goods sold on the weekend days continues to increase. The result can limit the ability of the DSD provider to synch with demand, leading to out-of-stocks.

According to the GMA report, 55% of survey manufacturing respondents indicated that they would be willing to deliver as needed (any day of the week) and 28% responded that they would be willing to add Saturday deliveries to improve in-stock positions. It says one major DSD supplier moved to a Saturday delivery schedule for a large mass merchant and saw multiple point sale increases from reducing out-of-stocks.

It is also possible the rise in fuel costs and increased “Green Supply Chain” initiatives will also serve as barriers to greater use of DSD. While no hard data exists, common sense says multiple carriers in smaller trucks delivering to each store will not be as fuel or carbon efficient as larger deliveries across vendors from a retail DC.

Indeed, in some areas Wal-Mart is moving away from DSD. In a highly publicized controversy in 2006, Coca-Cola had to battle lawsuits from many of its smaller PowerAde sports drink bottlers who fought plans for Coke to stop DSD on the beverage and instead ship larger quantities to Wal-Mart DCs for store delivery, which the retailer believes delivers greater total supply chain efficiencies. (See Suit over PowerAde Distribution Highlights Changes Dynamics in Beverage Distribution.) In a totally different retail area, Home Depot is dramatically reducing the amount of products its vendors ship direct to store in favor of DC shipments, for similar reasons.

In general, DSD is used where freshness is at a premium (bread, milk, salty snacks) or where the final product is produced very locally (beer, soft drinks). But it includes other categories such as cereal and cheeses, for example.

New Capabilities Required

There are two opportunities for growth in DSD. One is for manufacturers/distributors with existing DSD programs to expand those relationships with additional retailers and stores.

The other is to expand the number of categories and products that are supported by the DSD model.

In either case, manufacturers/distributors need to continue to advance their level of technology support. At the local driver/account manager level, for example, many have moved away from batch-based mobile terminals to real-time systems that connect directly to their back office inventory and sales systems.

Demand management and replenishment tools also need to be top notch.

“Cost-effectively servicing retail customers with a Direct Store Delivery model requires a single demand plan that provides both high-level and granular forecast visibility of time-phased volume by key distribution channels, customers, product lines and brands,” says Karin Bursa, VP of Marketing at Logility.

Do you expect to see DSD programs expand, shrink, or stay the same? Why? How can they be made more effective? Let us know your thoughts at the Feedback button below. |