SCDigest

Editorial Staff

| SCDigest Says: |

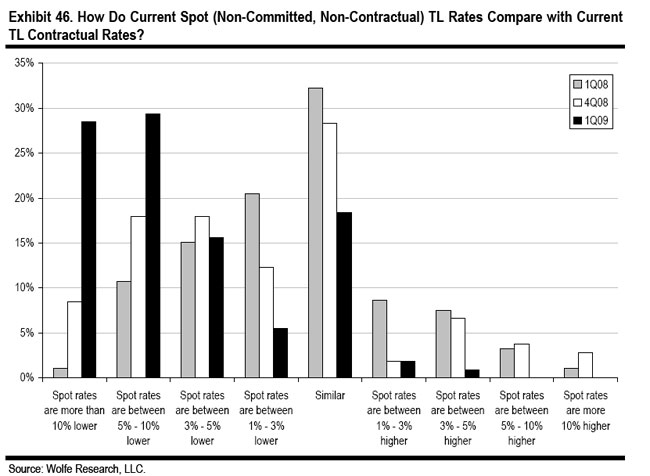

29% of respondents said that spot market truckload rates were 5-10% below there current contract rates, and another 28% who said spot rates were more than 10% lower. 29% of respondents said that spot market truckload rates were 5-10% below there current contract rates, and another 28% who said spot rates were more than 10% lower.

Click Here to See Reader Feedback

|

SCDigest was anxiously awaiting the Q1 shipper survey (now called “The State of the Freight”) from Ed Wolfe and Wolfe Research. The Q4 2008 report was certainly downbeat, but it was not clear if the full impact of the financial crisis had been captured in that quarter’s data.

Now we have the results for Q1 2009, where clearly the financial crisis and deep recession were fully felt by the hundreds of shippers that participate in the survey. The bottom line: more bad news for carriers in terms of falling volumes and rate expectations, but with some rays of hope that we have bottomed and that freight volumes and the overall economy will start to recover.

The bottom line, says Wolfe, is that “Despite increasing signs that the general economy and sentiment have not only stabilized but also recently have begin to improve, most freight signs point to continued deteriorating freight demand,” and that freight rates may not begin to move upward again until after 2010.

Key highlights from the report:

Transportation Budgets Shrinking in 2009: On average, shippers expect transportation budgets to drop a sharp 12% in 2009 without considering fuel, and 3.5% including fuel costs. Given the current level of fuel costs versus 2008, however, it seems to us that there is some disconnect between those two numbers.

Some Improvement in Expectations: While 63% of shippers expect to ship less in Q2 than they did in the same period for 2008, that’s actually down from 70% with those expectations in the last quarter’s survey. However, Wolfe notes they have not seen any uptick in freight volumes through April.

Some Movement from Rail to Truck: Other industry experts have noted that the extreme deals available in the truckload market are causing some shippers to move freight from rail to truck. The Wolfe survey supports this view, noting that “our survey results suggest that trucks will regain some modest market share back from rails over the next 6-12 months.” On a related note, the respondents on average see rail rates are about 11% lower than comparable truckload rates, the smallest delta since the survey began many years ago.

Lower Oil Prices Curb Intermodal Fervor: In Q3 2008, an astounding 80% of respondents said they were looking at moving some truckload movements to intermodal, mostly in response to then soaring fuel costs. In Q1, only 27% of respondents were looking to move more freight to intermodal.

Companies Delaying Inventory Builds: Even with signs of recovery, 70% of respondents do not think they will start to build inventories until at least Q3 2009, and 30% not until 2010.

(Transportation Management Article - Continued Below)

|