SCDigest

Editorial Staff

| SCDigest Says: |

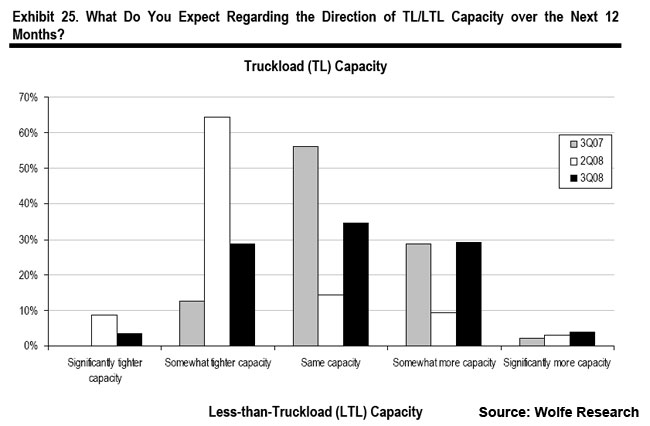

Probably in concert with perceptions of fewer carriers leaving the market, shippers in Q3 now see more over capacity in the truckload market, versus a small move towards seeing tightening capacity in Q2. Probably in concert with perceptions of fewer carriers leaving the market, shippers in Q3 now see more over capacity in the truckload market, versus a small move towards seeing tightening capacity in Q2.

Click Here to See Reader Feedback

|

We are always interested in the quarterly shippers survey and report, previously managed by transportation industry analyst Ed Wolfe and his team at Bear Stearns, now under his new company Wolfe Research.

Under the new title of “The State of the Freight,” the Q3 2008 survey results were released last week by Wolfe Research, and present an opportunity for interesting analysis. Wolfe says the survey was conducted prior to the end of September, when oil prices were at an average of $75 per barrel, and also before the US and global economy went into a deeper tailspin in October and November.

It will be interesting to see the results for Q4 2008 when they are released, probably in February, 2009.

For example, at $75 per barrel, fuel charges and related logistics costs were still very high versus those of just a couple of years ago. As a result, for example, 76% of Q3 respondents said that high fuel prices had caused them to consider less fuel-intensive transportation modes, such as rail and intermodal. Will that change in an environment of $50 per barrel oil? Maybe, but the current environment also places a premium on inventory reduction, which slower rail transport would less well enable.

Interestingly, the Q3 survey also found fewer shippers perceived that carriers were leaving the market versus the high levels of Q1 and Q2 of this year, as the inability, especially of smaller carriers, to fully recover soaring diesel fuel costs caused many of them to simply pull equipment off the road. While 51% saw some increase in truckload carriers exiting the market in Q3, that’s down from 73% in Q2. The proprietary Wolfe Research Truck Bankruptcy Index also has declined substantially from the levels of July. In both cases, the results may simply reflect that the weakest carriers left the market earlier in the year, and fewer of the remaining stronger carriers are going bust or giving up.

(Transportation Management Article - Continued Below)

|