SCDigest

Editorial Staff

| SCDigest Says: |

Shippers expect an effective 2008 base rate increase of just 0.4% and 0.8%, respectively, from their TL and LTL carriers, prior to fuel surcharges and accessorial costs. Shippers expect an effective 2008 base rate increase of just 0.4% and 0.8%, respectively, from their TL and LTL carriers, prior to fuel surcharges and accessorial costs.

What do you say? Send

us your comments here |

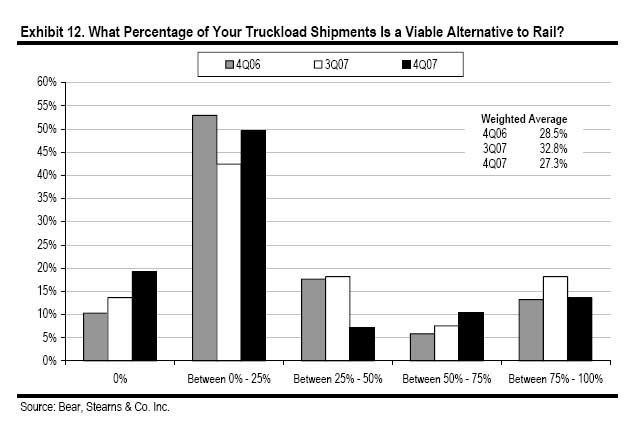

The always insightful Bear Stearns Quarterly Shippers Survey was released this week, covering responses from 200 shippers for the fourth quarter of 2007.

Since 2006, the survey has found consistently strong perceptions of heavy over-capacity in both the truckload and less-than-truckload (LTL) markets, and that continues again for the Q4 responses, but at declining rates. The report suggests that this could signal we are near a bottom in the supply-demand cycle in the transportation market.

While 65% of shippers believed in Q4 that there was overcapacity in the truckload market, that was actually down from an astounding 81% who felt so in Q3 2007 (a record level for the survey). In LTL, while 62% saw overcapacity in Q4, that was also down from 75% in Q3 2007.

“Anecdotally, we believe shippers’ Requests for Proposals (RFPs) in the market during early 2008 will look similar in scope to the record number of RFPs conducted in first-quarter 2007, as we believe shippers continue to try to take advantage of the soft environment to lock in flat to down rates in both TL and LTL,” the report’s authors, led by Ed Wolfe, write. “We also heard of several large shippers seeking to lock in two-year TL and LTL contracts rather than the typical one-year contract.”

(Transportation Management Article - Continued Below)

|