Since the bottom in mid-2009, US truckload rates have in general risen steadily, of late leading to rather strong levels of profitability for many of them, as a combination of also slow but steady increases in volumes plus generally strong asset discipline by carriers has moved the supply-demand balance in the truckers' favor.

But are those rate dynamics likely to continue, or is the trend line about to change?

The trend is in fact likely to change, according to respected transportation industry analyst John Larkin of Wall Street investment firm Stifel, Nicolaus & Company – but unfortunately not in the favor of shippers.

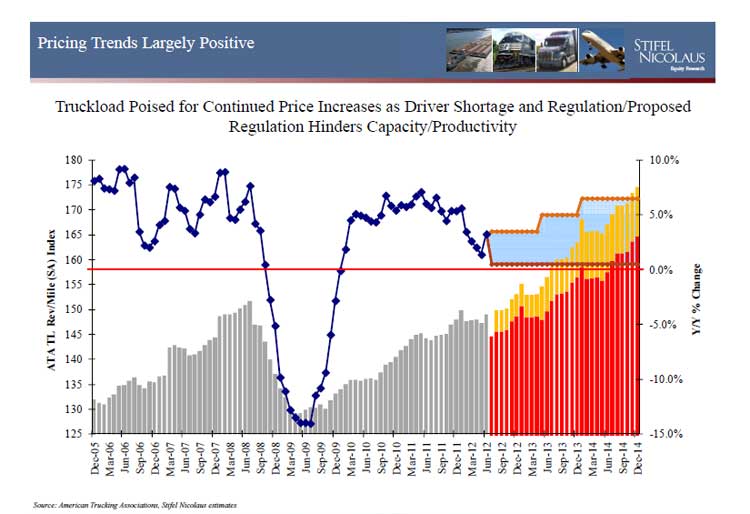

In a recent teleconference providing a sort of 360-degree view on freight transportation across modes, Larkin presented the following chart. It shows two sets of data over time: (1) Truckload revenue per mile, as represented by an index. For example, with a current level of about 148, revenue per mile is up about 14% from the low of 130 in 2009; and (2) the year over year change in that index.

Source: Stifel Nicolaus

Revenue per mile is not a perfect measure of actual rates, as other factors, such as better network utilization and lower deadheading, can impact the measure. Nevertheless, revenue per mile and rates in general change in tandem.

As can be seen, through the end of 2014, Larkin sees a sharp rise in the measure based on an scenario in which GDP grows jut modestly – 3% or so per year. GDP growth is the biggest driver of freight volumes, and volumes in turn along with capacity are the biggest drivers of rates.

As can be seen on the top line (reasonably optimistic GDP scenario), Larkin expects revenue per mile/rates to rise 3% for the second half of 2012, about 5% in 2013, and as much as 7% in 2016, or about 16% in total from where we were at the end of Q2 2012.

Why this sharp rise? A variety of factors. That includes a significant driver shortage, which could reach 250,000 by Q3 of 2012, Larkin says. That would create near crisis conditions as were seen in 2005.

“Gen Xers and Yers don’t want to drive trucks,” Larkins said.

Hours of Service changes and other regulations are serving to reduce driver and carrier productivity, lowering net capacity in the end.

Interestingly, shippers are in for it either way with regard to drivers. Either the shortage continues, meaning lower capacity will drive rates up, or carriers dramatically increase pay to lure more drivers back, but must pass those higher costs on to shippers.

Any Feedback on our Supply Chain Graphic of the Week? Let us know your thoughts at the Feedback button below.

|